AutoZone ($AZO)

A High Quality Auto Parts Retailer

Business Description

AutoZone is the largest retailer and distributor of automotive replacement parts and accessories in the Americas. It was founded in 1979 and currently operates 6,432 stores in the United States, 794 stores in Mexico, and 127 stores in Brazil. Their revenue can be split into two segments: DIY (do-it-yourself) and DIFM (do-it-for-me). The DIY business, which makes up 70% of total revenue, is AZO's bread and butter. The typical customers are men between the ages of 20 and 60, with below national median household income, who work on their cars out of economic necessity. On the DIFM side, the customers are local repair shops or mechanics who value delivery times and breadth of product inventory. An important thing to note about the business is that about 85% of revenues are composed of failure and maintenance-related products. Additionally, revenues are largely recession-resistant (2007 comps .1%, 2008 .4%, 2009 4.4%) as people end up deferring purchases of new cars during difficult times and choose to drive their old cars further by getting them repaired more frequently.

A great way to understand the business is to consider what the average customer visit looks like. Imagine something is wrong with your car, an essential piece of your livelihood, and getting it repaired by a mechanic or the dealership is unfeasible. You drive to the nearest aftermarket auto-part retailer because all you care about is getting your car working as fast as possible. In this case, it’s an AutoZone, which is a likely case as 90% of the U.S. population lives within 10 miles of a store. Within 30 seconds of entering the store or walking 30 feet, you get approached by a service member, a company policy. They try to address your problem with a huge database of info, looking up your make and model to find the exact part you need, costing $35 on average. The service member then teaches you all you need on how to install the part and lends you any tools required free of charge.

Industry Overview

From the previous example, the main factors AZO competes on become very clear: convenience, service, turnaround time, and inventory selection. What makes the business so attractive is that price is considered only after each of these factors is satisfied, reflected in their 50%+ and very stable gross margins, combined with very low variability in operating margin. These metrics suggest AZO is a high-quality and predictable business. Another thing that becomes clear is how crucial having a good supply chain is in ensuring the speed at which inventory can be moved.

Long-term drivers of the business are the fact that 1-2% more new cars are sold every year, while the average age of cars continually increases as cars are built better, resulting in average miles driven also increasing 1-2% per year. This leads to 3-4% underlying addressable market growth, which is very stable. Predictability in the market comes from the fact that the cars addressed by the aftermarket auto part industry are those out of warranty with the dealers. Industry standards for warranties are 7 years, so there is essentially a 7-year lead time on the addressable market. As the average age of a car rises, maintenance costs go up linearly with age. Another important industry dynamic is that the three biggest players control around 50% of the industry together (~20% AZO, ~17% ORLY, ~12% AAP), basically creating an oligopoly. Between all three, pricing is rational. They all understand the macroeconomic drivers behind the industry and acknowledge their underlying businesses generate very high ROIC. Barriers to entry are also very large as having such a huge assortment of products near customers, available at a moment's notice, requires incredible scale. Interestingly enough, store count for the entire industry has been relatively flat since 2000, while simultaneously, the big 4 (AutoZone, O’Reilly, Advance, and NAPA) have grown substantially, taking share from smaller competitors as they close their stores. I expect this trend to continue. As a whole, I expect consolidation to continue giving each player more scale, better distribution, and bargaining power, while the industry itself continues to grow at 3-4% per year.

Operations & Economics

A huge portion of AZO’s success has come from its ability to grow without retaining huge amounts of capital, a very rare characteristic for a retail business. The total store count has pretty metronomically increased by 200 per year for the last 10-15 years despite their reinvestment being opportunistic. During this time, capex has been around $500m per year. Per store, all-in startup costs are $2.5m (including central costs) and revenue around $2m, having grown at 5% in the recent past, while operating margin is consistently around 20%. This gives 15-16% returns from opening new stores. In reality, you could argue they are earning double that on a unit economics basis and when accounting for debt and capitalized leases. The overall business generates 40% ROIC, and over time, this figure has increased as incremental returns became more attractive. Another piece of AZO’s success has been through maintaining a negative working capital position to minimize capital employed. They do this by offsetting their high levels of inventory with payables, meaning their inventory is essentially funded by suppliers. Another crucial part of the business is its hub and spoke distribution model, which allows it to ensure every single store has adequate breadth and depth of inventory. This is done through mega hubs, or stores of 20,000 to 30,000 square feet, compared to regular stores, which are ~6600 square feet. The extra space is used to store additional inventory, allowing these stores to act as a mini distribution center for surrounding stores. This distribution capability and scale is their main competitive advantage, as inventory is a crucial part of this industry. On average, their inventory turns 1.5x every year, given that their specialty niche has incredibly high gross margins and inventory requirements compared to traditional retail businesses.

Shareholder Returns

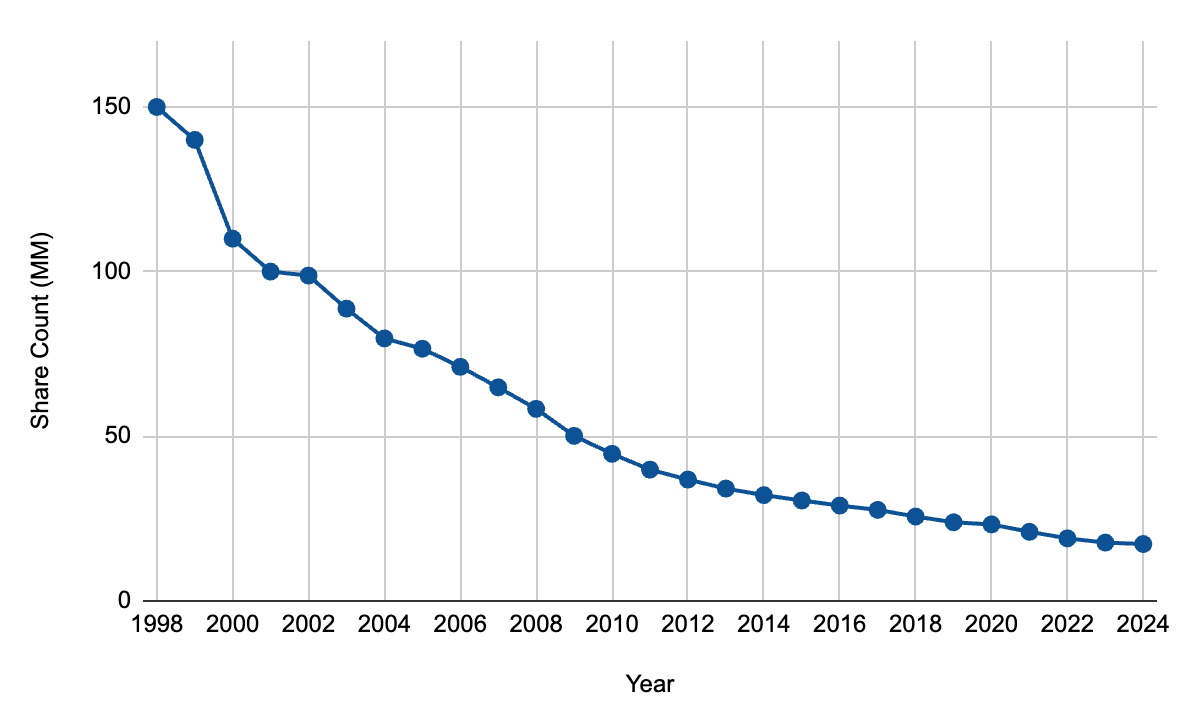

Although a usual thing to address, I think in AZO’s case, it’s important to consider the business history, as the stock has returned around 20% compounded for 30+ years. The main factor in this stellar performance has been the business momentum and the management team’s willingness to aggressively buy back their own shares, using around 93% of their operating cash flow, year after year. These shareholder returns have closely matched EPS growth over the same period, meaning that multiple expansion didn’t play much of a role. Breaking down the numbers further, they purchased an average of 8% of the shares outstanding every year since 2000, shrinking the total share count from 151m to 19m in just 24 years. This leaves 12% per year of underlying earnings growth from a mix of growing their store count and growing same-store sales.

As mentioned earlier, AZO operates in a mature, oligopoly industry where the growth is very stable. Management has a lot of certainty on how much the industry will grow and how their market share will change due to the macroeconomic drivers of the business being easily trackable and the ~7-year look ahead they have on the addressable market. Combine that with little capital intensity as inventory for new stores is financed by suppliers and 40%+ returns on capital from opening new stores, and you get an amazing recipe for outsized shareholder returns. Another great thing that AutoZone has done is consistently maintain a 2.5x Debt/EBITDA ratio by borrowing more money as EBITDA grows and using it to repurchase shares. Given how durable their cash flows are, this is a very healthy amount of net debt to keep on the business and allows them to retire even more shares.

Management Team

The main thing I like about AZO’s management is their very consistent strategy in terms of growing the business and allocating capital. Even going back to Bill Rhodes’ first year as CEO (2005), their rhetoric hasn’t changed much. Year after year, they have pretty much done the same thing, and it’s clearly been working well. Now, Rhodes has transitioned to Chairman, while Philip Daniele assumed the CEO position in January, after 30 years within AZO. After working under Rhodes for so long, he will likely keep doing much of the same. The company’s average CEO tenure of 9 years, almost double the median for the S&P 500, speaks to the strong culture. Another positive thing about the management team is that they place a huge value on honesty. One example is admitting their post-pandemic execution could have been better despite the business still performing well. In terms of compensation, Rhodes received $19m while Danielle and the other executions earned around $5-6m each, which is very reasonable. Each member of the management team is also required to hold shares worth many times their base salaries as the board would like to align incentives.

Growth Runway

Another important thesis point is the runway for growth AZO possesses, which will drive future results and serve as catalysts for higher share prices. A very key avenue for them is international expansion, particularly in Mexico and Brazil, where same-store sales growth has been in the high teens to 20% range for the last few years. Management is targeting opening ~200 stores annually in Mexico and Brazil by 2028, in addition to ~300 annual openings domestically. Although ambitious, given the store-level economics, 500 store openings per year could be an attractive upside scenario. In Mexico, AZO has a nearly 700 store lead on ORLY, giving them the first-mover advantage of more scale in a market where vehicle penetration should grow. On the other hand, ORLY is choosing to focus more of its efforts on Canada.

In addition to internal expansion, AZO has been making a significant push into the professional market (DIFM) market, where O’Reilly is currently the biggest player. Although I don’t foresee this changing, AutoZone should maintain its lead position in the DIY market while leveraging its existing distribution network to capture greater commercial share. We can see this in the 20% growth in AZO’s DIFM segment compared to a market that’s growing 4-5%. Although a theoretically lower gross margin business, the DIFM market remains relatively untapped and is ripe for further consolidation. This growth push makes a lot of sense for AZO as they are heavily concentrated in the DIY business, and over time, I foresee the DIFM segment becoming a greater portion of their revenues. Growing complexity in automobiles is likely to shift DIY customers to DIFM professionals; however, this shift will probably take multiple years as the fleet turns over with new models. This allows AutoZone to capture incremental growth in TAM as they enter the market, with their bigger store footprint and distribution network.

Risks

There are two threats to AZO's business that I feel need to be addressed. The first is e-commerce, becoming a greater share of aftermarket auto part sales through companies like Amazon. Although e-commerce is likely to grow as a percentage of sales, most customers will still choose to purchase their part in-store as the service component insulates it from online competition. An example of this is Rockauto.com, founded in 1999, which is an online retailer of aftermarket auto parts and maintains lower prices than even Amazon (~39% discount compared to the Big 4 and a ~22% discount to Amazon). Despite being around for so long, Rockauto has not posed much of a risk for AutoZone because competition in the industry is not very price-driven.

The second major threat, which I see as much more relevant, is a higher penetration of electric vehicles in the vehicle fleet, which are more complex to repair and have fewer moving parts. This means DIY customers will slowly transition to DIFM customers while the overall addressable market may decrease. AutoZone’s shift into the DIFM market to more closely compete with ORLY is very important as it insulates them more from this risk. Additionally, EV penetration will take much longer than most people expect, as the cohorts of people most receptive towards purchasing them already have due to cost subsidizing. The people yet to purchase EVs are going to transition much more slowly, and I think ICE vehicles are here to stay for the foreseeable future. Overall, I still expect AZO to continue growing despite these headwinds due to continuing industry consolidation and international expansion into markets with stronger tailwinds. But it’s important to acknowledge the threat they pose to the business’ long term success, and if you were to research AutoZone yourself, you would need to develop a view on these risks.

Thesis & Valuation

My overall view surrounding AutoZone is “business as usual”. I don’t foresee anything drastic happening and actually expect quite the opposite. I like the durability and predictability of AutoZone’s cash flows, incredible incremental returns on capital, and consistent capital allocation. Of course, if they accelerate store openings, EPS will grow faster, and the result should be better for shareholders, assuming that they hit their 15% hurdle rate. A key area to monitor is their execution in improving their distribution through utilizing more mega hubs in their model. Through their location network, they have a huge advantage over other competitors in an industry where there will always be more than one winner. This means AZO doesn’t necessarily have to be the best in the industry, it just has to have distribution and service that places it amongst the top few competitors.

Finally, my thoughts on valuation are very simple. The consensus is for EPS growth of around 10-14% annually, consisting of 5-7% share repurchases and 5-7% earnings growth, derived from 3-4% growth in same-store sales and 2-3% new store openings. The current earnings yield of ~5% seems fair given these qualities, but also leaves room for multiple expansion to speed up your returns. I think the opportunity for 10%+ returns lies in AZO’s underappreciated predictability, long runway for growth, and narrative around how EVs and e-commerce are near-term existential risks for the business despite not materializing for the foreseeable future. All things considered, I view AZO as a great business that requires (and has) a great management team, at a very reasonable price. It’s a nice balance between paying up a little for better business quality while also making sure multiple contraction isn’t a major headwind. However, it is still a little pricy for my liking, so I will probably add it to my watchlist and revisit the thesis if it trades at a lower multiple. My ratings for this AutoZone are 8/10 on business quality, 5.5/10 for valuation with my overall interest level being a 6.5/10.